Lumibot¶

Build, backtest, and run algorithmic trading strategies and AI agents in Python.

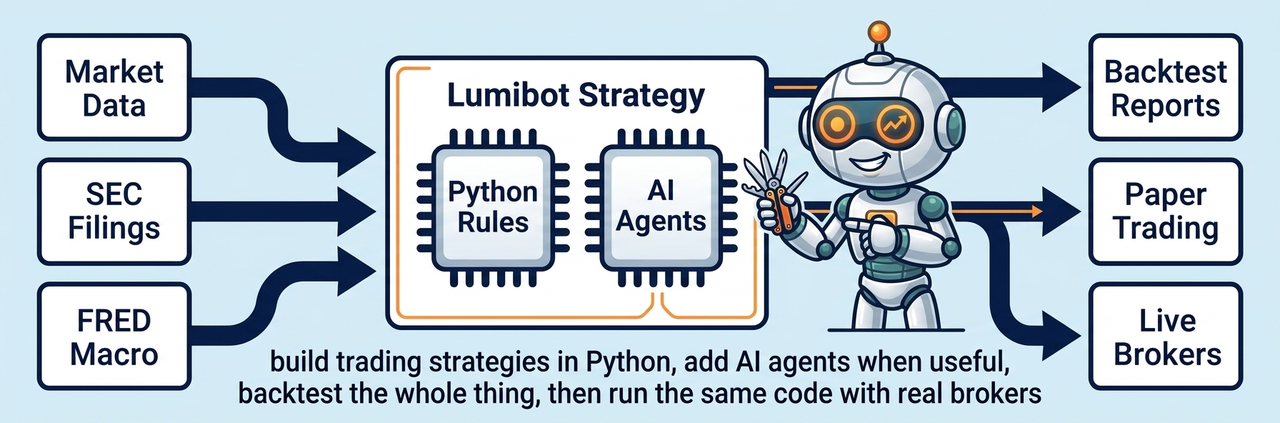

Lumibot is a Python framework for building deterministic strategies, AI trading teams, and hybrid trading systems that backtest, paper trade, and run live through real brokers.

Use normal Python for rules, indicators, schedules, position sizing, and risk controls. Add AI agents when you want a strategy to research market data, SEC filings, macro data, news, technical indicators, and account state before making a decision.

The same strategy lifecycle works from historical backtests to paper trading and live trading, so you can inspect behavior before connecting a real account.

Lumibot also supports AI trading agents inside the strategy lifecycle, including DuckDB-powered time-series analysis, external MCP tools, replayable agent runs, and trading permissions that keep research agents read-only.

Getting Started¶

After you have installed Lumibot on your computer, you can create a strategy and backtest it using free data available from Yahoo Finance, or use your own data. Here’s how to get started:

Step 1: Install Lumibot¶

Note

Ensure you have installed the latest version of Lumibot. Upgrade using the following command:

pip install lumibot --upgrade

Install the package on your computer:

pip install lumibot

Step 2: Create a Strategy for Backtesting¶

Here’s some code to get you started:

from datetime import datetime

from lumibot.backtesting import YahooDataBacktesting

from lumibot.strategies import Strategy

# A simple strategy that buys AAPL on the first day and holds it

class MyStrategy(Strategy):

def on_trading_iteration(self):

if self.first_iteration:

aapl_price = self.get_last_price("AAPL")

quantity = self.portfolio_value // aapl_price

order = self.create_order("AAPL", quantity, "buy")

self.submit_order(order)

# Pick the dates that you want to start and end your backtest

backtesting_start = datetime(2020, 11, 1)

backtesting_end = datetime(2020, 12, 31)

# Run the backtest

MyStrategy.backtest(

YahooDataBacktesting,

backtesting_start,

backtesting_end,

)

Step 3: Take Your Bot Live¶

Once you have backtested your strategy and understand how it behaves on historical data, you can take your bot to paper trading or live trading. Notice how the strategy code is exactly the same. Here’s an example using Alpaca (you can create a free Paper Trading account here in minutes: https://alpaca.markets/).

from lumibot.brokers import Alpaca

from lumibot.strategies.strategy import Strategy

from lumibot.traders import Trader

ALPACA_CONFIG = {

"API_KEY": "YOUR_ALPACA_API_KEY",

"API_SECRET": "YOUR_ALPACA_SECRET",

"PAPER": True # Set to True for paper trading, False for live trading

}

# A simple strategy that buys AAPL on the first day and holds it

class MyStrategy(Strategy):

def on_trading_iteration(self):

if self.first_iteration:

aapl_price = self.get_last_price("AAPL")

quantity = self.portfolio_value // aapl_price

order = self.create_order("AAPL", quantity, "buy")

self.submit_order(order)

trader = Trader()

broker = Alpaca(ALPACA_CONFIG)

strategy = MyStrategy(broker=broker)

# Run the strategy live

trader.add_strategy(strategy)

trader.run_all()

Important

Remember to start with a paper trading account to ensure everything works as expected before moving to live trading.

AI Trading Team¶

LumiBot is built for AI agents that reason, call external tools, and make trading decisions on every bar during a backtest – then run the exact same code live. This is real agentic backtesting: the LLM is inside the simulation loop, not bolted onto the side.

Classic Python strategies are still first-class. LumiBot lets you choose the right level of intelligence: fixed rules, AI agents, or a hybrid where Python handles the hard gates and agents reason through evidence.

Backtest AI trading agents with real external data from 20,000+ MCP servers

LLM in the loop on every bar – the agent reasons over point-in-time market state, calls tools, and submits orders

Replay caching makes warm backtest reruns deterministic and fast (zero LLM calls on rerun)

Any LLM provider per agent – use a cheaper model for evidence gathering and a stronger model for debate/trading

Built-in SEC fundamentals and filings – agents can inspect income statements, balance sheets, cash flow, company facts, and annual reports

Built-in FRED macro data – agents can inspect rates, inflation, labor, growth, liquidity, credit spreads, and market-risk series

Trading permissions – research agents can use read-only tools while portfolio-manager agents place orders

Same code for backtest and live – write once, backtest it, deploy it

External MCP servers are just a URL – no local scripts, no npm installs

Key AI agent docs:

AI Trading Agents and Agentic Backtesting – main guide: agentic backtesting framework, MCP trading tools, and competitive positioning

Design Your AI Trading Team – design single-agent, multi-agent, debate, team, and hybrid flows

AI Trading Team Examples – copy-paste AI trading team examples, including leveraged ETFs, large-cap stocks, Ray Dalio idea meritocracy, Warren Buffett value, Bill Ackman concentrated, and Citadel sector pods

SEC Fundamentals – SEC fundamentals and filing research tools

FRED Macro Data – FRED macro data tools and point-in-time behavior

Agent Built-In Tools – built-in tools, indicators, and trading permissions

AI Agents Quick Start – quick start with code examples for AI agent backtesting

Canonical AI Agent Demos – three reference demos: news sentiment, macro risk, and M2 liquidity

AI Agent Observability – traces, replay cache, warnings, and debugging workflow

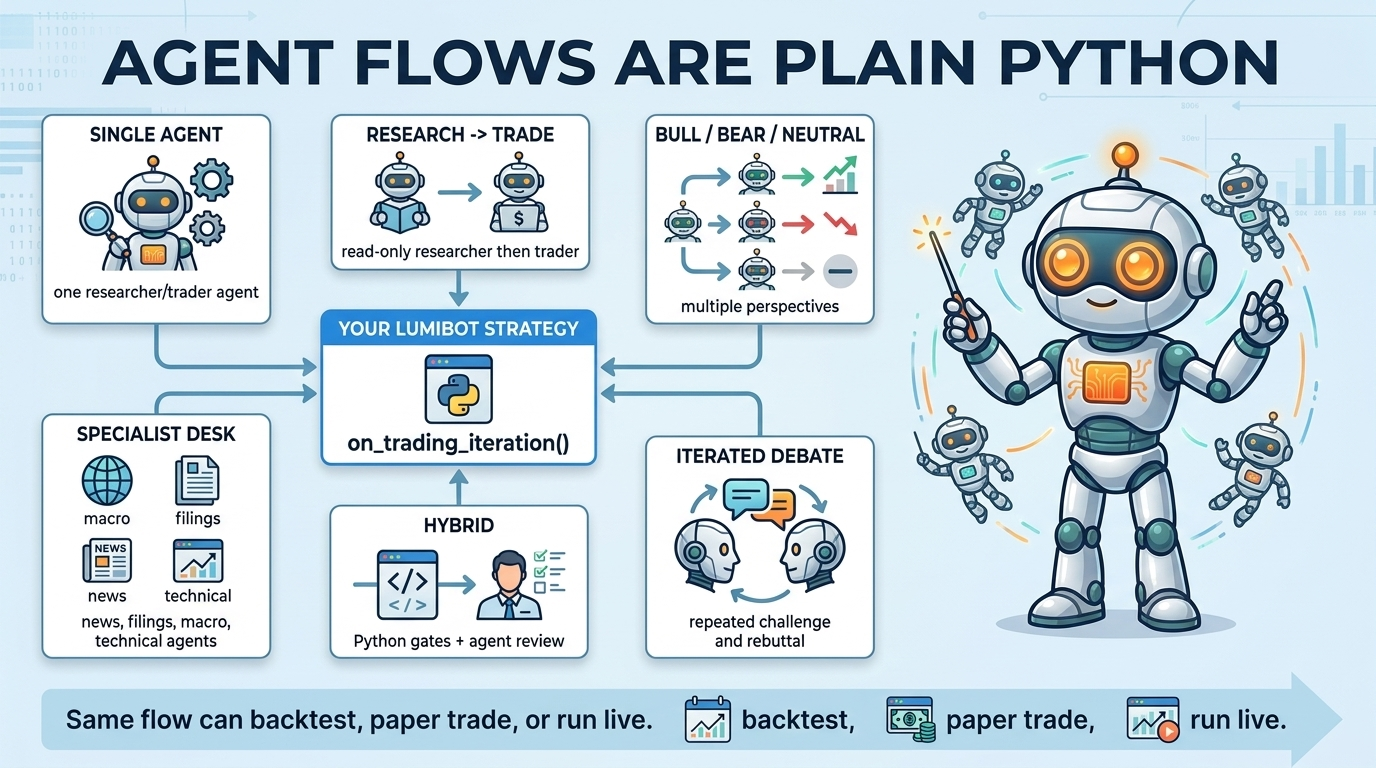

Design Your AI Trading Team¶

An AI trading team is just a group of agents with different jobs inside the same LumiBot strategy. You can build a single-agent strategy, a specialist research flow, bull/bear/neutral teams, model-vs-model debates, deterministic execution gates, or agent reviewers layered on top of normal Python logic.

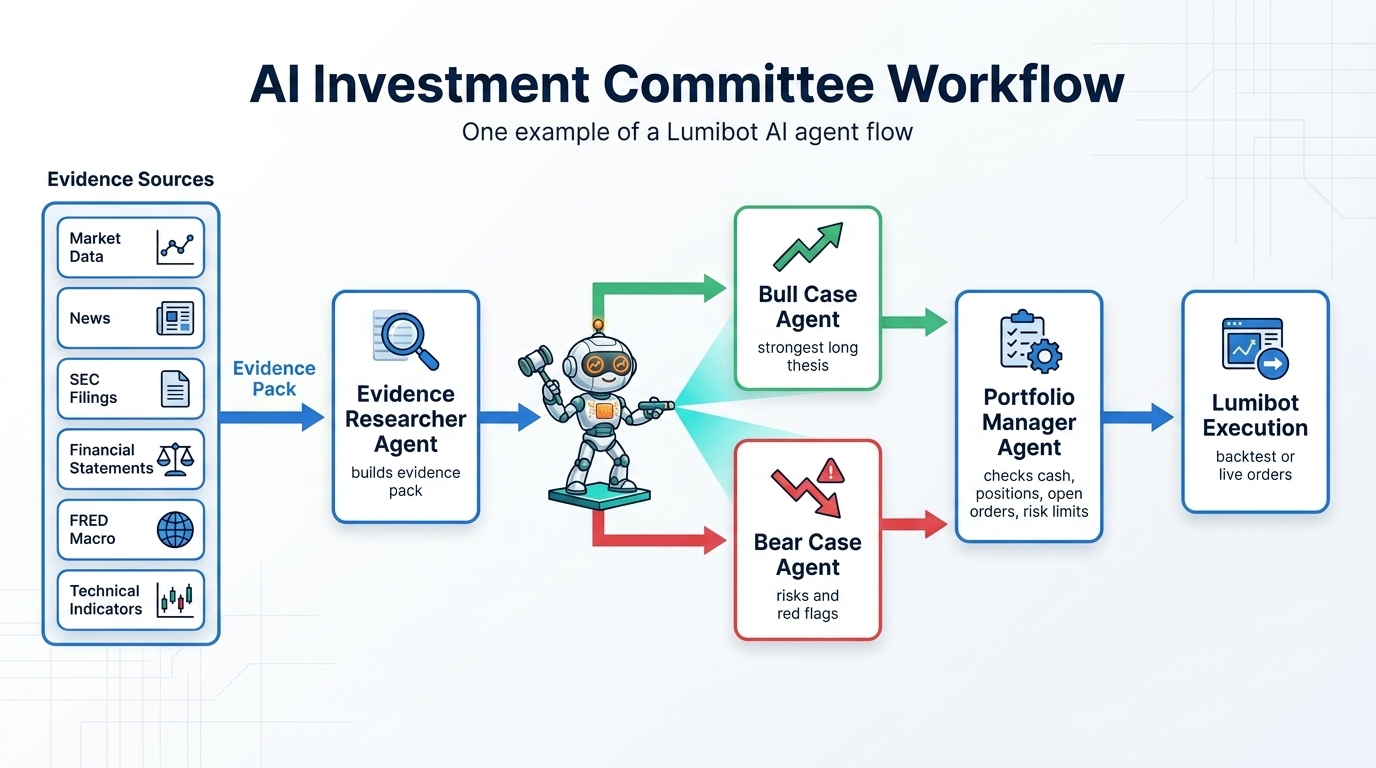

Example: Research, Bull, Bear, and Trader Agents¶

Here is one example pattern: a researcher gathers evidence, bull and bear agents debate the trade, and a trader agent decides what to buy or sell.

In this pattern, each agent has a job:

Research Agent: builds the evidence pack from market data, filings, fundamentals, news, macro data, and indicators.

Bull Agent: turns that evidence into the strongest long thesis.

Bear Agent: challenges the thesis, looks for risk, and argues for avoiding, delaying, or reducing the trade.

Trader / Portfolio Manager Agent: checks cash, positions, open orders, and risk limits, then decides whether to trade.

The copy-paste example below implements that exact team. It uses Gemini Flash Lite because it is fast and inexpensive for experiments.

To run it with a broker in paper mode, set your AI and Alpaca credentials and run the file:

export GEMINI_API_KEY='your-key-here'

export ALPACA_API_KEY='your-alpaca-key'

export ALPACA_API_SECRET='your-alpaca-secret'

export ALPACA_IS_PAPER=true

python ai_trading_team_bull_bear_leveraged_etf.py

To backtest the same strategy instead, change IS_BACKTESTING = False to IS_BACKTESTING = True in the runner:

export GEMINI_API_KEY='your-key-here'

python ai_trading_team_bull_bear_leveraged_etf.py

Save this as ai_trading_team_bull_bear_leveraged_etf.py. If an AI key is missing or invalid, LumiBot stops and prints a clear provider key error with a link to create a key.

import os

from datetime import datetime

from lumibot.strategies.strategy import Strategy

class AITradingTeamBullBearLeveragedETFStrategy(Strategy):

parameters = {

"universe": ["TQQQ", "SQQQ", "UPRO", "SPXU", "UDOW", "SDOW", "TNA", "TZA", "TECL", "TECS", "SOXL", "SOXS", "WEBL", "WEBS", "FAS", "FAZ", "LABU", "LABD", "ERX", "ERY", "GUSH", "DRIP", "DRN", "DRV", "TMF", "TMV", "NUGT", "DUST"],

}

def initialize(self):

self.sleeptime = "1D"

model = os.environ.get("AI_TRADING_TEAM_MODEL", "gemini-3.1-flash-lite")

# The first three agents are read-only. They can reason, but cannot trade.

self.agents.create(

name="researcher",

model=model,

allow_trading=False,

system_prompt="Rank the ETFs by upside. Be direct.",

)

self.agents.create(

name="bull",

model=model,

allow_trading=False,

system_prompt="Argue for the strongest money-making trade.",

)

self.agents.create(

name="bear",

model=model,

allow_trading=False,

system_prompt="Point out the biggest risk, briefly.",

)

# Only this final agent can submit orders through Lumibot.

self.agents.create(

name="trader",

model=model,

allow_trading=True,

system_prompt="Buy one ETF from the universe aggressively. Use nearly all cash.",

)

def on_trading_iteration(self):

# Each trading day, pass the same market context through the team.

context = {

"date": self.get_datetime().date().isoformat(),

"universe": self.parameters["universe"],

}

research = self.agents["researcher"].run(

task_prompt="Pick the strongest ETF.",

context=context,

)

bull = self.agents["bull"].run(

task_prompt="Make the bull case.",

context={**context, "research": research.summary},

)

bear = self.agents["bear"].run(

task_prompt="Make the bear case.",

context={**context, "research": research.summary, "bull": bull.summary},

)

self.agents["trader"].run(

task_prompt="Sell anything that is not the pick, then buy the best ETF with nearly all available cash.",

context={**context, "research": research.summary, "bull": bull.summary, "bear": bear.summary},

)

if __name__ == "__main__":

IS_BACKTESTING = False

if IS_BACKTESTING:

from lumibot.backtesting import YahooDataBacktesting

AITradingTeamBullBearLeveragedETFStrategy.backtest(

YahooDataBacktesting,

datetime(2026, 4, 7),

datetime(2026, 5, 22),

)

else:

from lumibot.brokers import Alpaca

from lumibot.traders import Trader

ALPACA_CONFIG = {

"API_KEY": os.environ["ALPACA_API_KEY"],

"API_SECRET": os.environ["ALPACA_API_SECRET"],

"PAPER": os.environ.get("ALPACA_IS_PAPER", "true").lower() != "false",

}

broker = Alpaca(ALPACA_CONFIG)

strategy = AITradingTeamBullBearLeveragedETFStrategy(broker=broker)

trader = Trader()

trader.add_strategy(strategy)

trader.run_all()

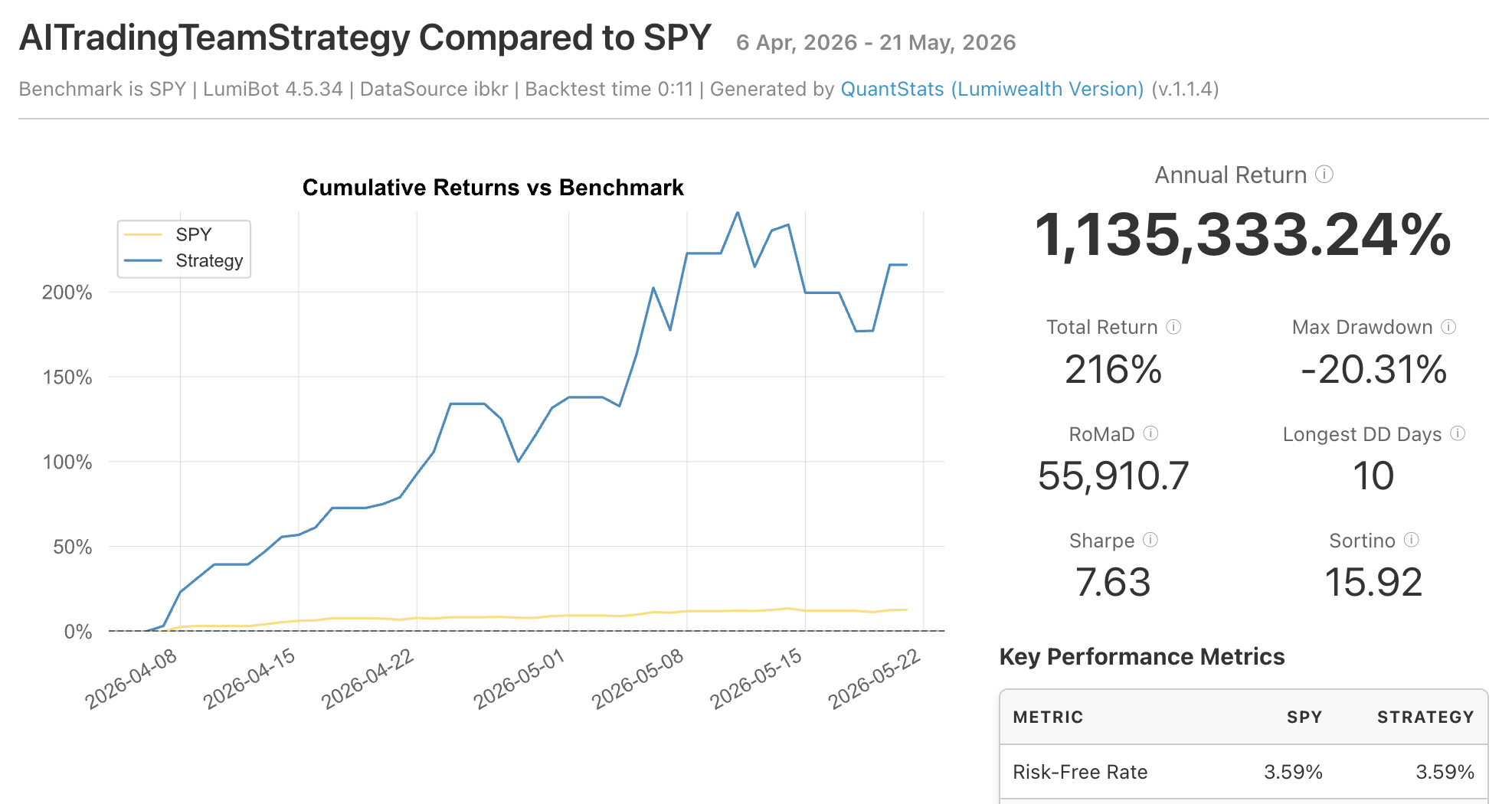

Example backtest artifact from this sample strategy:

The result is intentionally eye-catching, but the exact percentage is not the point. The point is that the full AI trading team runs inside Lumibot’s normal broker and backtest loops, so the decisions, orders, and artifacts are inspectable before you connect real money. Backtests are not expected future performance.

More AI Trading Team Examples¶

These examples show different ways to organize an AI trading team. Each page explains the inspiration, the agent flow, how to run it with a broker in paper mode, and how to backtest it.

Citadel Sector Pods AI Trading Team – inspired by the pod-style structure associated with Ken Griffin’s Citadel: sector specialists pitch their best ideas, a risk manager challenges crowding and drawdown risk, and a portfolio manager rotates into the strongest sector ETF. Watch it live on BotSpot.

Warren Buffett Value AI Trading Team – uses AI agents like a patient value-investing desk: one agent digs into business quality and annual reports, one demands valuation discipline, and the portfolio manager only buys the best long-term compounder. Watch it live on BotSpot.

Ray Dalio Idea Meritocracy AI Trading Team – turns Bridgewater-style thoughtful disagreement into a macro ETF workflow, with growth, inflation, liquidity, and disagreement agents arguing before the trader acts. Watch it live on BotSpot.

Bill Ackman Concentrated AI Trading Team – inspired by Pershing Square-style concentrated investing: find one great business, make the activist bull case, attack it like a short seller, then let the portfolio manager take a focused position if the thesis survives. Watch it live on BotSpot.

Bull/Bear Leveraged ETF AI Trading Team – a fast, aggressive demo where bull and bear agents debate leveraged long and inverse ETFs before the trader rotates into one high-conviction ETF. Watch it live on BotSpot.

Bull/Bear Large-Cap Stocks AI Trading Team – the same debate structure applied to familiar large-cap stocks, which makes it easier to inspect each agent’s reasoning before using more volatile instruments. Watch it live on BotSpot.

Cash Accounting¶

Lumibot supports explicit cash accounting for both backtests and live broker telemetry. Use the strategy cash methods for deposits, withdrawals, direct cash adjustments, and financing setup, then review the resulting cash-adjusted returns in the standard backtest artifacts.

Backtests keep external cashflows out of strategy performance

Live cloud payloads can include normalized broker

cash_eventsListener storage keeps raw normalized events in a dedicated event table

Start with Cash Accounting for the end-to-end guide.

Additional Resources¶

If you would like to learn how to modify your strategies, we suggest that you first learn about Lifecycle Methods, then Strategy Methods, and Strategy Properties. You can find the documentation for these in the menu, with the main pages describing what they are, then the sub-pages describing each method and property individually.

We also have some more sample code that you can check out here: https://github.com/Lumiwealth/lumibot/tree/dev/lumibot/example_strategies

Next, explore the AI agent docs if you want a strategy that researches evidence, debates bull and bear cases, checks risk, and trades from the same Python lifecycle.

Need Extra Help?¶

If you want a guided path instead of piecing everything together from docs, start with the AI Trading Bootcamp. It teaches the full workflow: turn an idea into a Lumibot strategy, backtest it, inspect the artifacts, connect a broker, and decide when it is ready for paper or live trading.

BotSpot is the cheaper, easier way to run Lumibot once you want hosted data, parallel backtests, broker connections, monitoring, alerts, audit history, and scheduled deployment without maintaining your own trading server.

Learn the full workflow

The AI Trading Bootcamp is the fastest path if you want guided help building Lumibot strategies with AI. Learn how to structure a strategy, run a backtest, read the artifacts, connect a broker, and decide what should happen before anything trades live.

Why run Lumibot on BotSpot?

BotSpot removes the infrastructure work around the strategy when you are ready to build, test, or run it in the cloud:

- Hosted data and artifacts: backtest without assembling every data feed yourself.

- Parallel backtests: compare strategy variants on BotSpot servers instead of tying up your laptop.

- Cheaper scheduled runs: run periodic bots without paying for always-on infrastructure per strategy.

- Broker connections and monitoring: keep logs, charts, alerts, account checks, audit history, and kill switches in one place.

- MCP tools: let Codex, Claude Code, Cursor, and other coding agents launch backtests, inspect artifacts, and prepare runs.

Why Lumibot?¶

AI trading projects have proved that people want agentic trading workflows. Lumibot’s edge is that those workflows run inside a real Python trading framework. You can backtest the agent decisions, inspect the artifacts, add normal Python guardrails, paper trade, and connect to brokers without rewriting the strategy.

That matters because an AI trading demo is not the same thing as a trading system. Without backtests and broker-aware strategy code, you are mostly trusting prompts. Lumibot lets you iterate faster: test the agent flow on historical data, see what it would have bought or sold, tighten the Python risk checks, then run the same lifecycle in paper or live trading.

Compared With AI Trading Agent Projects¶

Project |

AI trading teams |

Backtest decisions |

Paper/live broker path |

Hosted deploy/monitoring |

|---|---|---|---|---|

Lumibot + BotSpot |

Flexible teams, single agents, debates, hybrid flows, and deterministic gates |

Yes: replayable decisions, orders, traces, artifacts, charts, logs |

Yes: Alpaca, IBKR, Tradier, Schwab, Tradovate, ProjectX, Bitunix, selected CCXT |

Yes: hosted data, parallel backtests, deployment, monitoring, MCP, alerts, kill switches |

TradingAgents |

Yes, focused on a specific multi-agent research structure |

Research/demo oriented |

Not the main focus |

No |

ai-hedge-fund |

Yes, focused on named investor-style agents |

Demo/backtest oriented |

Not the main focus |

No |

OpenAlice |

Yes, one-person Wall Street agent concept |

Experimental |

Local/self-run focus |

No |

QuantDinger |

Yes |

Yes |

Crypto, IBKR, MT5, Alpaca |

Self-hosted |

Vibe-Trading |

Yes, personal trading agent flow |

Yes |

Agent platform focus |

Platform-specific |

AI-Trader |

Yes |

Platform focus |

Platform focus |

Platform-specific |

OpenBB |

Tooling for agents |

Not a strategy backtester |

No broker execution framework |

OpenBB platform |

Qlib |

Research/ML agents |

Quant research backtests |

Limited live focus |

No |

Read the detailed comparison page: AI Trading Project Comparison.

Polymarket Trading And Backtesting¶

LumiBot supports Polymarket prediction-contract trading and backtesting through the normal broker, data-source, and

backtesting abstractions. Strategies can search markets, resolve outcomes to CLOB token ids, read order books and

quotes, inspect market rules and resolution status, backtest historical Polymarket prices, and submit live orders using

create_order and submit_order.

Start with the full setup and reference guide: Polymarket.

Compared With Backtesting Libraries¶

Library |

Same code: backtest + live |

Assets |

AI agent runtime |

Broker/live path |

Hosted deployment |

|---|---|---|---|---|---|

Lumibot |

Yes |

Stocks, options, crypto, futures, forex, prediction markets |

Built-in |

Alpaca, IBKR, Tradier, Schwab, Tradovate, ProjectX, Bitunix, Polymarket, selected CCXT |

BotSpot |

Backtrader |

Yes |

Stocks, limited crypto/futures, outdated forex |

No |

IB only/outdated |

No |

Freqtrade |

Crypto |

Crypto |

FreqAI/ML |

Crypto exchanges |

No |

Zipline |

No |

Stocks |

No |

None |

No |

Backtesting.py |

No |

Stocks, crypto, futures, forex |

No |

None |

No |

vectorbt |

No |

Stocks, crypto, futures, forex |

No |

No |

No |

NautilusTrader |

Yes |

Stocks, crypto, futures, forex, limited options |

No |

Exchange adapters |

No |

Hummingbot |

Crypto |

Crypto market making |

Scripts/controllers |

Crypto exchanges |

Ecosystem/enterprise options |

Table of Contents¶

- Home

- Build and Deploy with BotSpot

- BotSpot MCP Integration

- GitHub

- Reddit Community

- Discord Community

- Getting Started

- Imports and Startup

- AI Trading Agents and Agentic Backtesting

- AI Agents Quick Start

- Design Your AI Trading Team

- AI Trading Team Examples

- Agent Built-In Tools

- Canonical AI Agent Demos

- AI Agent Observability

- Agent Memory

- Agent Notifications

- Why This Is Different

- Quick Start

- How

@agent_toolWorks - External Data Patterns

- Built-in Tools

- System Prompts

- Agent Handoffs

- DuckDB and Time-Series Data

- Replay Cache

- Observability

- Canonical Demos

- Frequently Asked Questions

- Error Handling and Reliability

- AI Trading Project Comparison

- Cash Accounting

- Lifecycle Methods

- Summary

- def initialize

- def on_trading_iteration

- def before_market_opens

- def before_starting_trading

- def before_market_closes

- def after_market_closes

- def on_abrupt_closing

- def on_bot_crash

- def trace_stats

- def tearsheet_custom_metrics

- def on_new_order

- def on_partially_filled_order

- def on_filled_order

- def on_canceled_order

- def on_parameters_updated

- Strategy Methods

- Strategy Properties

- Entities

- Indicators

- SEC Fundamentals

- FRED Macro Data

- Backtesting

- Brokers

- Reference

- Code Examples

- Deployment Guide

- Option A — Deploy on BotSpot (Recommended)

- Option B — Self-hosted Deployment (Render or Replit)

- Example Strategy for Deployment

- Choosing Your Self-hosted Platform

- Deploying to Render

- Deploying to Replit

- Secrets Configuration

- Broker Configuration

- Tradier Configuration

- Tradovate Configuration

- Alpaca Configuration

- Coinbase Configuration

- Kraken Configuration

- Additional CCXT Exchange Examples

- Interactive Brokers Configuration

- Interactive Brokers-Legacy Configuration

- Schwab Configuration

- Bitunix Configuration

- DataBento Configuration

- ProjectX Configuration

- General Environment Variables

- Final Steps

- Conclusion

- Common Mistakes and How to Avoid Them

- Frequently Asked Questions (FAQ)

- Get Pre-Built Strategies