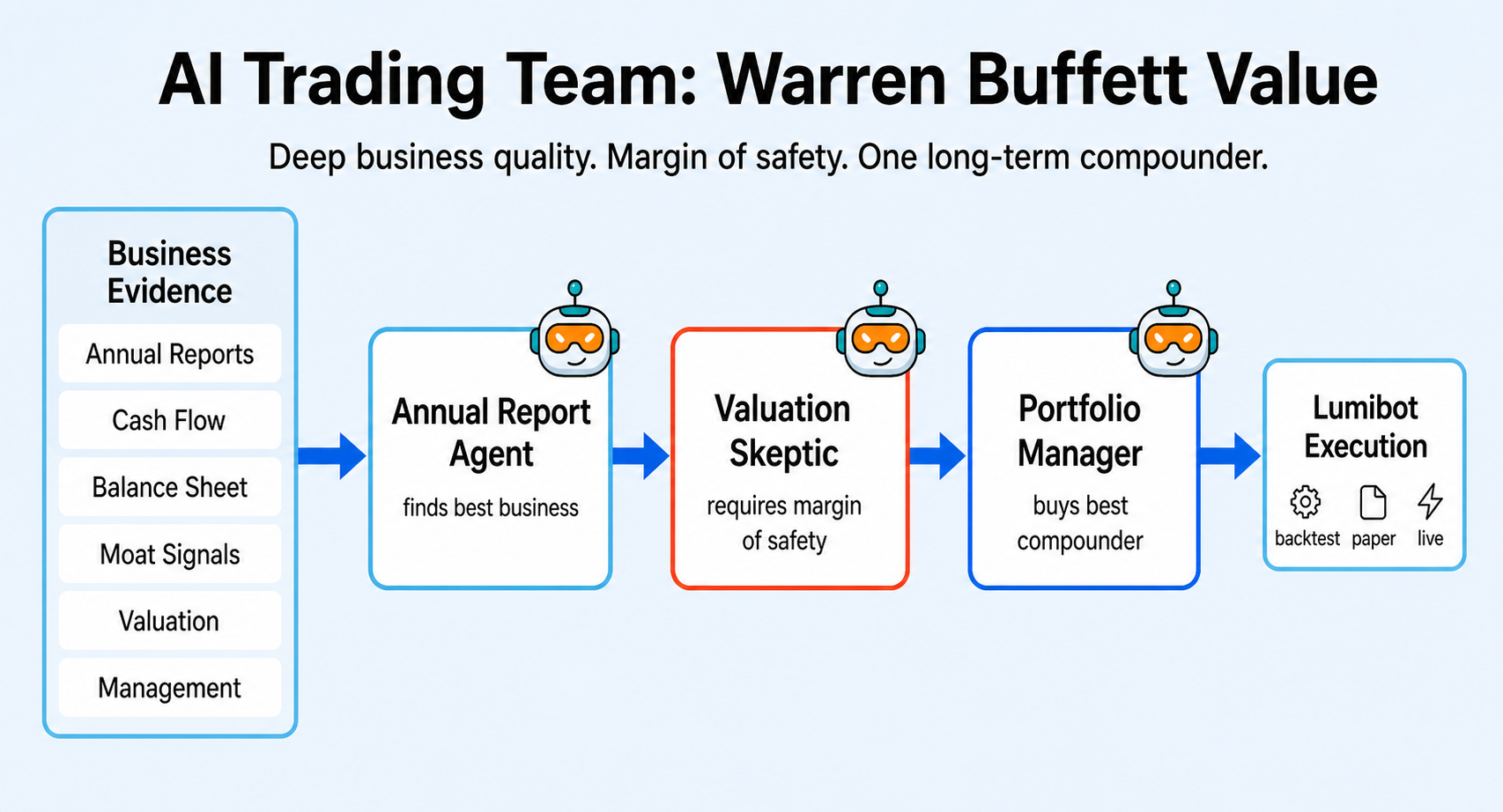

Warren Buffett Value AI Trading Team¶

This strategy is inspired by Warren Buffett’s public investing style: understand the business first, read the filings, care about durability, avoid overpaying, and only act when the idea is strong enough to own. The point is not to clone Buffett. The point is to show how AI agents can divide a value-investing process into research, skepticism, and final portfolio action.

The first agent behaves like an annual-report reader. It looks for business quality, cash generation, balance-sheet strength, and durability. The second agent plays valuation skeptic and asks whether the price still leaves a margin of safety. The portfolio manager only trades if the business-quality case and valuation discipline both survive.

See this strategy running live on BotSpot

How the team works¶

annual_report_readerstudies business quality, cash flow, filings, and durability.valuation_skepticchallenges valuation and asks for a margin of safety.portfolio_managerbuys the best long-term compounder and is the only agent allowed to trade.

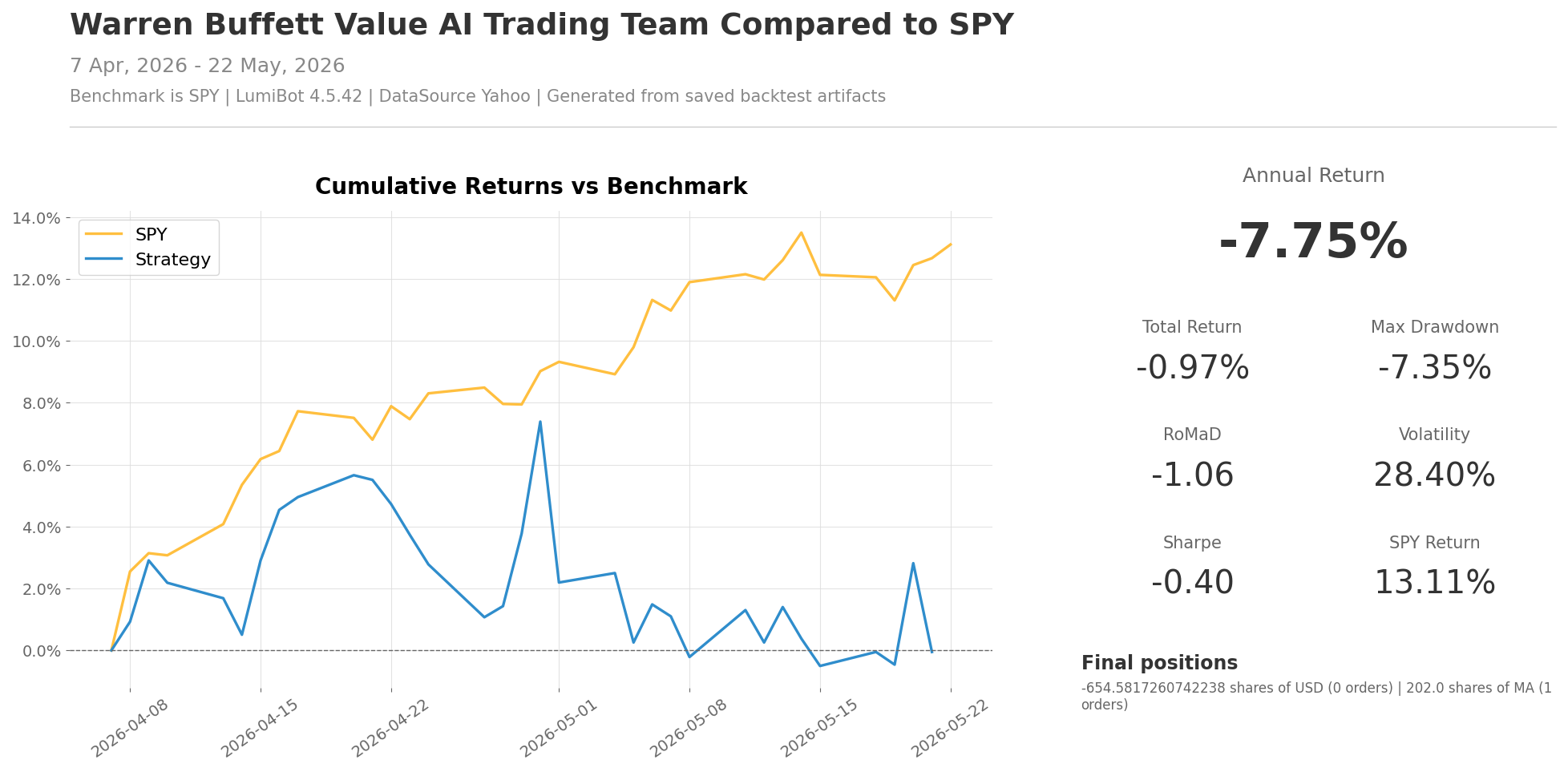

Backtest snapshot¶

Run it with a broker¶

The file defaults to broker-connected execution. With Alpaca, it runs in paper

mode unless you set ALPACA_IS_PAPER=false.

export GEMINI_API_KEY='your-key-here'

export ALPACA_API_KEY='your-alpaca-key'

export ALPACA_API_SECRET='your-alpaca-secret'

export ALPACA_IS_PAPER=true

python lumibot/example_strategies/ai_trading_team_warren_buffett_value.py

Backtest it¶

Use the same strategy class and change IS_BACKTESTING = False to IS_BACKTESTING = True in the runner:

export GEMINI_API_KEY='your-key-here'

python lumibot/example_strategies/ai_trading_team_warren_buffett_value.py

Example code¶

"""Warren Buffett-inspired annual-report value AI trading team example.

This example is inspired by public Berkshire Hathaway shareholder letters and

value-investing principles. It is not affiliated with or endorsed by Warren

Buffett, Berkshire Hathaway, or related companies.

Set GEMINI_API_KEY plus Alpaca credentials, then run paper trading:

python ai_trading_team_warren_buffett_value.py

Set IS_BACKTESTING=True in the runner to run the historical example instead.

"""

import os

from datetime import datetime

from lumibot.strategies.strategy import Strategy

class AITradingTeamWarrenBuffettValueStrategy(Strategy):

parameters = {

"universe": ["AAPL", "MSFT", "GOOGL", "COST", "V", "MA", "KO", "AXP", "JPM", "PG"],

}

def initialize(self):

self.sleeptime = "1D"

model = os.environ.get("AI_TRADING_TEAM_MODEL", "gemini-3.1-flash-lite")

self.agents.create(

name="annual_report_reader",

model=model,

allow_trading=False,

system_prompt="Find the best business quality from filings, fundamentals, cash flow, balance sheet strength, and durability.",

)

self.agents.create(

name="valuation_skeptic",

model=model,

allow_trading=False,

system_prompt="Challenge the business-quality case. Require a margin of safety and reject weak or overpriced ideas.",

)

self.agents.create(

name="portfolio_manager",

model=model,

allow_trading=True,

system_prompt="Buy the best long-term compounder from the universe when quality and margin of safety are acceptable. Use nearly all cash.",

)

def on_trading_iteration(self):

context = {

"date": self.get_datetime().date().isoformat(),

"universe": self.parameters["universe"],

}

report = self.agents["annual_report_reader"].run(task_prompt="Pick the highest-quality business.", context=context)

skeptic = self.agents["valuation_skeptic"].run(

task_prompt="Challenge the valuation and business-quality case. Require margin of safety.",

context={**context, "report": report.summary},

)

self.agents["portfolio_manager"].run(

task_prompt="Sell anything that is not the best long-term compounder, then buy the best stock with nearly all available cash.",

context={**context, "report": report.summary, "skeptic": skeptic.summary},

)

if __name__ == "__main__":

IS_BACKTESTING = False

if IS_BACKTESTING:

from lumibot.backtesting import YahooDataBacktesting

AITradingTeamWarrenBuffettValueStrategy.backtest(

YahooDataBacktesting,

datetime(2026, 4, 7),

datetime(2026, 5, 22),

)

else:

from lumibot.brokers import Alpaca

from lumibot.traders import Trader

ALPACA_CONFIG = {

"API_KEY": os.environ["ALPACA_API_KEY"],

"API_SECRET": os.environ["ALPACA_API_SECRET"],

"PAPER": os.environ.get("ALPACA_IS_PAPER", "true").lower() != "false",

}

broker = Alpaca(ALPACA_CONFIG)

strategy = AITradingTeamWarrenBuffettValueStrategy(broker=broker)

trader = Trader()

trader.add_strategy(strategy)

trader.run_all()